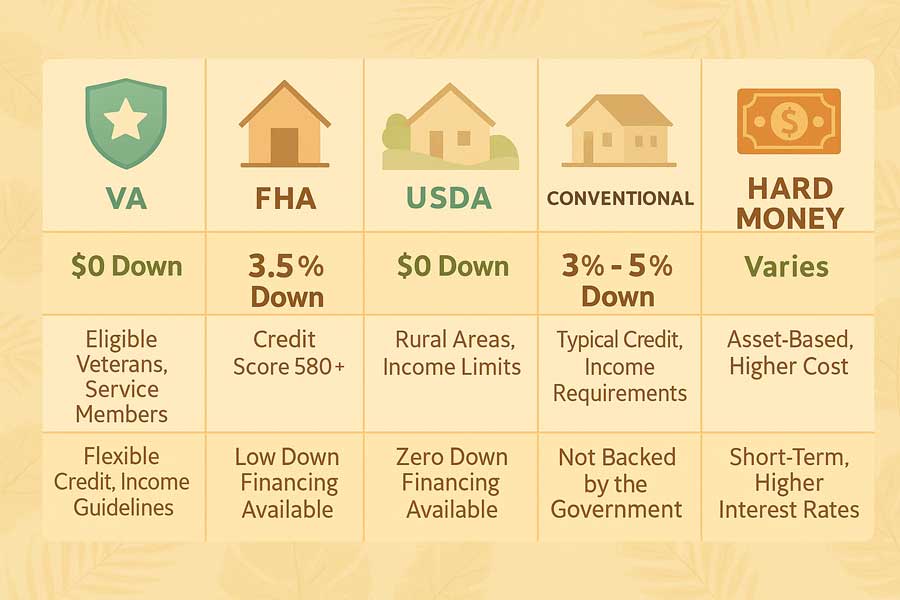

It’s no secret that navigating the homeownership journey can seem daunting. But if you’re a veteran, National Guard, or service member and qualify for the VA home loan, it offers you a golden pathway to your dream home here in paradise. This step-by-step guide describes the process and sheds some light on the Hawaii VA home loan process, as well as provides a detailed walkthrough of the VA home loan process and tips to streamline it for your convenience.

Let’s dive in!

VA Loan Process: 9 Steps (Hawaiʻi)

Step 1: Obtain Your Certificate of Eligibility (COE)

Your journey begins by obtaining your Certificate of Eligibility (COE). The COE verifies to lenders that you meet the necessary service requirements for a VA loan. You can obtain your COE through the VA’s website, or you can contact our team, and we can pull your COE for you.

Step 2: Pre-qualification

After obtaining your COE, the next step is prequalification. It is a preliminary evaluation of your financial status to gauge how much you might be eligible to borrow. You fill out an application, give permission to pull credit, and discuss how much you are looking to borrow with your lender. Getting a pre-qualification gives borrowers an idea of how much they can afford, but in order to place an offer on a property, you need to complete step 3.

Step 3: How to Get Preapproved for a VA Home Loan

Next is the pre-approval stage. Getting pre-approved means you have submitted an application and given your mortgage professional supporting documentation. The lender will analyze the information provided and verify the information given in the loan application. A pre-approved VA buyer means sellers can rest assured the VA buyer will have no issues prequalifying va loan up to the pre-approved amount.

Step 4: House Hunting

Knowing how much you can borrow is essential to ensuring you are looking for homes within your budget. Now, you’re equipped to go house hunting! At this stage, your mortgage professional will step back and work with your realtor on tailoring the pre-approval letter for any specific offers our VA buyers will want to make.

Step 5: The Purchase Agreement

Once you’ve found your dream home, you’ll make an offer and negotiate the terms until both parties agree. This agreement will be outlined in a purchase contract.

Step 6: Home Inspection

After the contract is signed, an inspection and VA appraisal will be conducted to ensure the home’s value and condition meet the VA’s standards. While an inspection is not required, it is a good idea, as often, inspectors will catch many things that an appraiser might miss. The home inspection is often scheduled a few days after contract acceptance, and after receiving the report, members utilizing their Hawaii VA home loan typically have 2-4 days to accept the condition of the property or to reach an agreement on seller credits and/or repairs to be made to the property. Once the inspection is completed and VA buyers accept the report, the appraisal is ordered.

Step 7: Initial Disclosures, Loan processing, & VA appraisal

A loan estimate and initial disclosures are sent to the VA borrowers. These are signed and allow the mortgage professional to then order the VA appraisal. An appraisal is always required for members utilizing their Hawaii VA home loan for purchasing or doing a VA Cash-out refinance. Currently, the cost is a $900 flat fee in Hawaii, regardless of if the appraiser is appraising a 3000 sq ft home or a 600 sq ft condo. This is often the longest part of the process, but the loan is submitted to underwriting for conditional approval while the appraisal is in queue to be completed.

Step 8: Conditional Approval / Final Approval

You can get a conditional approval in as little as one to two days, compared to the past when it would take 90 days. The underwriters will review documents, ensure accuracy of income, verify assets, and when the underwriters have confirmed the loan meets all necessary requirements, the underwriting team will issue a conditional approval. These conditions can range from obtaining updated pay stubs or bank statements to submitting letters of explanation for large deposits in the VA borrowers’ bank statements.

After meeting the conditions, including receiving the appraisal and receiving a Notice of Value (NOV) for a dollar amount above the contract price, the loan will be submitted for final approval. When your loan officer submits your loan for final approval, they will often order Closing Disclosures at the same time. Closing disclosures are an updated loan estimate that gives the VA buyer more fidelity on final numbers. There is a 3-business-day waiting period after buyers sign their Closing Disclosures.

Step 9: Closing

Congratulations! The last step is closing, where all the loan documents will be signed, and the keys to your dream home will be handed over to you. This process typically takes 4-5 days. Borrowers will sign the loan documents, which will be uploaded and reviewed, and after the loan is funded (1-2 days after signing), Hawaii buyers wait 2 days until the loan is recorded with the local government. Buyers receive the keys to their house on the recording date.

What to Expect at Each Stage of the VA Home Loan Process

Navigating the VA loan process can be exciting and challenging, but knowing what to expect at each stage will make your journey smoother.

During the COE, prequalification, and pre-approval stages, anticipate documentation and financial checks. You’ll need documents proving your military service, income, and credit history. It’s crucial to have an excellent real estate agent to ensure the terms are favorable. The inspection and VA appraisal might seem nerve-wracking, but they’re there to protect you from overpaying or purchasing a home with severe defects. Lastly, you can expect to sign a pile of documents at the closing stage. But don’t worry, at the end, you’ll have your keys to your home in paradise!

Tips to Streamline the Process

While the VA loan process might seem overwhelming, there are ways to streamline the journey to buying a home.

Tip 1: Get Your Documents in Order

Before starting the process, gather all the necessary documents. These include your proof of service (DD214), income verification (pay stubs), and last two months of bank statements.

Tip 2: Work with a VA Loan Specialist

Working with a VA loan specialist can ensure that the process runs smoothly. Their experience and knowledge can be invaluable in guiding you through each stage. Although in many areas VA loans are simpler, there are many different rules/regulations with regard to counting income, boarding income, credit requirements, etc. Further, a VA loan specialist will be able to ask you specific questions which other mortgage professionals might not even know to ask ie. will you still be getting sea pay, are you on shore duty, etc.

Tip 3: Maintain Your Credit Score

A good credit check score is vital for a pre-qualification and pre-approval for the maximum loan amount possible. A bad credit score might not prevent you from using your VA home loan entitlement, but it could lower your pre-approval amount by hundreds of thousands. Make sure to pay bills on time and keep credit card balances low to maintain a good score and receive the best interest rates possible.

Special Option for Native American Veterans: The NADL Program

Before we wrap up, it’s worth highlighting a unique benefit available to eligible Native American veterans: the Native American Direct Loan (NADL) program. This VA-backed option is designed specifically for purchasing, building, or improving homes on federal trust land, and it often comes with lower closing costs compared to traditional loans.

To qualify, you must meet certain eligibility requirements, such as confirmed VA loan entitlement and residence on tribal trust land. Your tribal government must also have an agreement (MOU) with the VA. If you meet these criteria, the NADL can provide a more affordable path to homeownership with the support of the VA.

Now that you have a clear picture of the full VA loan process

How to Get Pre-Approved for a VA Home Loan

Pre-approval shows sellers you’re fully vetted and ready. Most borrowers can get a VA pre-approval letter in about 1–3 days with complete documents.

What your lender reviews

- COE (Certificate of Eligibility) — proves VA eligibility and entitlement

- Credit — a soft or hard pull, depending on the lender

- Income — pay stubs/LES (BAH/BAS if active-duty), W-2s/1099s, tax returns as needed

- Assets — bank statements for reserves/closing costs

Documents checklist

- Government ID + SSN

- DD214 (Veterans) or Statement of Service (active duty/Guard/Reserve)

- Recent pay stubs/LES and two months of bank statements

- Last two years W-2s/1099s (and tax returns if self-employed)

Estimate My VA Pre-Approval | Get My COE

How Long Does the VA Loan Process Take?

In Hawaiʻi, most VA buyers close in about 30–45 days once you’re under contract. Here’s the typical range by stage.

| Stage | Typical Time (Hawaiʻi) | What moves it faster |

|---|---|---|

| COE retrieval | Instant–1 day | Lender pulls via ACE; records match |

| Pre-approval | 1–3 days | Complete docs; quick responses |

| House hunting | 1–4+ weeks | Pre-approval letter; clear budget |

| Offer → acceptance | 1–3 days | Strong terms; proof of funds |

| Appraisal ordered | Day 3–5 after acceptance | Order immediately; flexible access |

| Underwriting (conditional) | 2–5 days | Clean file; rapid doc turn |

| Clear conditions + NOV | 3–10 days | Fast appraisal corrections; complete MCAs |

| Closing Disclosures | 3 business days | Early e-consent and review |

| Sign, fund, record | 1–2 days | Schedule early; wire funds on time |

VA Loan Process Timeline (Day-by-Day)

- Day 0–1: Get COE, submit application, credit pull, upload docs.

- Day 1–3: Receive pre-approval letter; begin showings with agent.

- Day 4–10: Offer accepted; lender orders VA appraisal; disclosures signed.

- Day 11–20: Appraisal inspection; underwriting issues, conditional approval.

- Day 21–30: Clear conditions (VOE, assets, insurance, any appraisal updates); NOV issued.

- Day 31–35: Receive Closing Disclosure (3-day wait starts); schedule signing.

- Day 36–45: Sign, fund, and record. Keys!

Note: Turn times vary with market volume, condo approvals, and appraisal access. Your lender will keep your timeline tight with early orders and same-day condition turns.

VA Pre-Qualification vs Pre-Approval

| Pre-Qualification | Pre-Approval | |

|---|---|---|

| What it is | Informal estimate from a brief review | Document-verified lender review |

| Credit/docs | May not be pulled or verified | Credit pulled; income/assets reviewed |

| Letter | Usually no letter | Pre-approval letter for offers |

| Strength | Good for planning | Stronger with sellers |

| Best use | Early budgeting | Active house hunting & offers |

Run a VA pre-approval estimate or start your pre-approval.

FAQs

What is the VA loan process?

A step-by-step path from COE and pre-approval to house hunting, offer, appraisal/underwriting, and closing. Most Hawaiʻi buyers close in about 30–45 days once under contract.

How to get preapproved for a VA home loan?

Apply with a VA lender, authorize credit, upload income/asset docs, and provide your COE. Many borrowers receive a pre-approval letter in 1–3 days.

How long does the VA loan process take?

Pre-approval: 1–3 days with complete docs. Contract-to-close: typically 30–45 days in Hawaiʻi, depending on appraisal turn time and underwriting conditions.

What’s the difference between pre-qualification and pre-approval?

Pre-qualification is an informal estimate; pre-approval is a document-verified review that produces a letter you use for offers.

Can I get pre-approved without a COE?

You can start, but you’ll need the COE to close. Most lenders can pull it instantly via the VA portal when records match.

How long is a VA pre-approval letter good for?

Typically 60–90 days; your lender can refresh it with updated docs if needed.

What can slow down the timeline?

Missing documents, appraisal access delays, condo project issues, or major credit changes. Responding quickly and ordering early keeps things moving.

Conclusion

Understanding what to expect and implementing these tips can make the process smoother and more manageable. As your guide on this journey, we’re here to assist you every step of the way. Let Elias help you navigate through this process-whether you’re wondering how the VA home loan process works or you’re ready to start the journey, Elias is here to guide you.